Profit and loss statements explained (+ templates and examples)

Wouldn’t it be great if you could know what the future holds for your business?

Well, you kind of can, and we aren’t talking about magic here!

What we’re referring to is the profit and loss statement (P&L), which gives you insight into how well your business is doing. Or how badly, for that matter.

In fact, experts consider a profit and loss statement one of the most common financial documents in any sector and business plan. You may even call it mission-critical.

In this in-depth guide, we’ll cover the essential elements of profit and loss statements, including:

- Profit and loss statements most common types,

- Examples of profit and loss statements,

- Profit and loss statement templates,

- Tested tips for making better P&L statements, and more.

Let’s start with a few general remarks that you need to know first!

Table of Contents

What is a profit and loss statement?

A profit and loss statement is a financial statement that typically covers the following items:

- Revenues,

- Costs, and

- Expenses.

Moreover, a profit and loss statement usually consists of company revenues, costs, and expenses within a specific period, like a month, a quarter, a fiscal year — or even a week.

When done properly, a P&L can help protect the financial bottom line of a company by offering deeper insights into how a business can reduce costs and increase revenue.

In other words, a profit and loss statement is a handy tool that allows you to scrutinize the financial health (or lack thereof) of your company.

Interestingly, a P&L statement goes by many names, depending on the experts you talk to. Here’s a quick list of some of the terms:

- Expense statement,

- Statement of profit and loss,

- Income statement, etc.

In any case, P&L statements summarize a company’s revenues, expenses, and costs in one form or another and are typically performed by in-house or outsourced accountants. But, if you’re a finance-savvy manager, you can even perform one yourself — at least the less detailed P&L statements.

Sidenote: Public companies are required by law to make their P&L statements publicly available — specifically, on their web page’s investor relations section.

Because of the insight they offer, profit and loss statements allow managers, leaders, and investors to make better investing decisions or spot underperforming business areas.

To get you on the same page with creating your P&L statements the right way, let’s take a quick look at 2 universal methods for creating profit and loss statements.

2 Universal methods for creating a P&L statement

A profit and loss statement comes into existence thanks to 2 types of accounting methods — either the accrual method or the cash method. In simple terms, these universal accounting methods are tools for tracking and recording expenses in certain ways.

Still, the method you choose can make all the difference.

For illustration, investors often inspect corresponding types of P&L statements published by same-sector companies of similar size. After crunching the numbers, they spot trends in managing expenses and decide to invest in one company rather than another.

For clarity’s sake, suppose a company decides to use the cash method, although using the accrual method would have provided more insight into the company’s financial performance. In this case, the investors may disapprove of the inappropriate use of accounting methods, leading to the investor deciding not to invest in the company.

To explore further, we’ll next discuss the accrual and cash method in more detail.

Accounting method #1: Cash method

Accountants often call this “the cash accounting method.” Companies use the cash method only when they need to record instances of cash changing hands — that is, when cash actually enters or leaves the business.

An example of this would be if a business counts their cash on hand and the money they paid for expenses.

Accountant Francis Fabrizi of Keirstone Limited explained that smaller companies typically prefer the cash method of accounting:

“Some small businesses may choose to use the cash method for accounting purposes, as the accrual method can be more complex and time-consuming to use.”

Yet, this approach comes with a major downside, as it accounts for cash only when it is either paid or received.

Accounting method #2: Accrual method

Unlike the cash method, the accrual method records profit only when it’s earned. In a nutshell, this means that a company records expenses or revenue after the service has been provided, regardless of the fact that it hasn’t received the cash for offering the service.

Simply put, companies typically use the accrual method for funds that they expect to receive at a future date.

In the subscription age, the accrual method is a much-loved method for recording revenue and sales.

For example, picture an on-demand streaming service like HBO GO or Netflix. These companies use the accrual method to record revenue on their P&L statements, although they haven’t collected the payment for the service — but expect to receive it at a given subscription renewal period.

In fact, the accountant we mentioned previously, Francis Fabrizi, clarified that the accrual-based method is the preferred method for financial accounting:

“The reason is that the accrual method provides a more accurate picture of a company’s financial performance. This is because it recognizes revenue and expenses in the period in which they are actually incurred, rather than when cash is exchanged. The accrual method helps to ensure that revenues and expenses are matched in the same accounting period.”

—

As we have seen, the cash and accrual methods of accounting come with their pros and cons. So, choose the one that fits your needs, your company’s reporting, and your client’s requirements.

🎓 Clockify Pro Tip

Whichever accounting method you pick, bear in mind that the process of collecting data for your profit and loss statement is best done using accounting software. Take a look at some of the best on the market:

What is the structure of a profit and loss statement?

By now, you might wonder what is in a profit and loss statement. To answer your question, the structure of a typical P&L statement looks something like this:

- Revenue: the total amount of money that the business has earned during a given accounting period (a week, month, quarter, calendar year, or fiscal year).

- Cost of goods sold (COGS): the cost of the services or products sold by the company; includes items like materials and direct labor.

- Gross profit: the difference between revenue and cost of goods sold; also known as gross margin and gross income.

- Operating expenses: the cost of operating the company, including rent, utilities, payroll, general and administrative costs; includes anything not covered by the cost of goods sold.

- Operating income: the difference between gross profit and operating expenses; shows how much profit a business makes from its activities prior to deducting interest and taxes.

- Non-operating items: interest expenses, interest income, gains or losses from selling assets, and other non-operating expenses or non-operating income.

- Net income, net profit, or bottom line: the profit after the company has deducted all expenses; represents the company’s final figure or overall loss or profit for the corresponding period.

Sure, with all this information in mind, a P&L statement may not infuse you with enthusiasm, but it’s critical that you still prepare it regularly.

Anyway, don’t worry about it — we’ll provide you with a few examples and templates that’ll help you craft your own profit and loss statement. But before we get into that, let’s check out a few common types of P&L statements.

🎓 Clockify Pro Tip

Explore the difference between gross salary and net salary in our blog post:

What are the common types of profit and loss statements?

For your convenience, here’s a list of a few types of P&L statements you can use, depending on whether you’re a small, medium, or large company.

| Name of the statement | How it benefits your business | Ideal for |

|---|---|---|

| Single-step P&L statement | Calculates net income by deducting total expenses from total revenue in a single step | Smaller companies, like service companies and sole proprietorships |

| Multi-step P&L statement | Breaks down expenses into categories like operating expenses and cost of goods sold, giving a thorough insight into financial performance | Complex, large businesses, like construction companies and factory facilities |

| Comparative P&L statement | Lets you compare your current revenues, costs, and expenses with those in prior financial statements | Any-sized companies, including small, medium, and large businesses |

| Pro forma P&L statement | Enables you to forecast the financial status of your company under speculative circumstances | Any-sized companies, including small, medium, and large businesses |

| Contribution margin P&L statement | Helps you see how particular products or services contribute to the profit of your business | Any-sized companies, including small, medium, and large businesses |

| Consolidated P&L statement | Provides a snapshot of the financial performance across the business’s subsidiaries | Mid-sized and large companies |

Regardless of the period for which you choose to implement your P&L statement — weekly, monthly, quarterly, or yearly — make sure to pick the right format from the list above that fits your company preferences and needs.

Speaking of time periods, we’ll next explore 2 criteria that you must not lose sight of when creating your profit and loss statement.

2 Criteria to consider before crafting a P&L statement

At this point, you need to know some types of P&L statements can be extraordinarily simple, and others can be incredibly complex. Certainly, some of them fall somewhere in between, and we’ll get to those.

For now, we can classify types of profit and loss statements based on 2 criteria:

- Period the statement covers, and

- Depth of data the statement provides.

In essence, we can refer to them as periodic and detailed P&L statements, but the actual format varies based on a company’s preferences and reporting standards.

Let’s go over each of those 2 criteria of profit and loss statements in more detail.

Criterion #1: Period the statement covers

In terms of timeframes, P&L statements are categorized into 4 types:

- Weekly P&L statements allow you to get a sneak preview of your company’s financial health for the past week,

- Monthly P&L statements deliver insight into a company’s profitability or losses in the course of a calendar month,

- Quarterly P&L statements illustrate financial performance (or lack thereof) over a 3-month period, and

- Yearly P&L statements provide a snapshot of a company’s financial performance over the span of a fiscal year.

Make sure you choose one or more for optimal business results — because, in contrast, a lack of periodic P&L statements can stifle your business growth.

For instance, even though people may be queueing up in front of your business to buy your product, that doesn’t necessarily mean that you’re making great profits. In fact, only after conducting a periodic P&L statement can you compare your profits with your costs.

Understandably, all P&L statements need to cover some period of time, whether a week, month, or year. So, let’s consider the depth of your profit and loss statement next.

Criterion #2: Depth of data the statement provides

You can divide the types of profit and loss statements in terms of the depth they go into to describe the financial status of a company.

Rule of thumb — the more depth you go into, the better your chances of spotting inconsistencies and issues.

In short, a smaller company can easily analyze its bottom line with the single-step profit and loss statement. In contrast, a large multinational corporation may need to turn to a comparative profit and loss statement for maximum benefits.

For example, elaborate P&L statements can benefit companies looking to cut their general expenses, like amortization and depreciation costs, when they conduct a profit and loss statement.

Depreciation and amortization refer to the practice of estimating the value of company assets over time. Yet, some businesses neglect to factor in these items, leading to failure in projecting long-term growth.

—

With these important criteria out of the way, let’s explore 3 examples to make the process of creating profit and loss statements more tangible.

Examples of a profit and loss statement

Now you’re familiar with the structure and types of P&L statements — kudos!

So, let’s dive into a few real-world scenarios where you can implement P&L reporting. For illustration, here are the 3 profit and loss statement examples we’ll cover:

- Small bakery P&L statement,

- Product/service company P&L statement, and

- Restaurant P&L statement.

Let’s up your financial game with a few real-life examples!

#1 Example of profit and loss statement: Small bakery

Suppose you want to start a business in Alabama, and you decide it’s going to be a small bakery. For a while, you successfully operate your company. After a few months, it’s high time you requested a profit and loss statement to be done to assess how well you’re doing.

In this case, you’ll use the single-step P&L statement because it neatly and simply analyzes the bottom line of a small business. For this example, it suffices to use the cash method of accounting, as this method records instances when cash actually enters or leaves the business.

To start things off in the right direction, begin by looking at baked goods and beverages — that’s the entire company revenue at this stage. How much the bakery makes and sells, i.e., your revenue, impacts the financial bottom line.

Next, you need to consider costs, like utilities, wages, and ingredients. Finally, you’ll get the net income that depicts the loss or profit of the business for the given period.

For practical purposes, we’ll offer a simplified version of the single-step P&L statement for your small bakery.

Note that the list of revenue items and costs listed below isn’t exhaustive, as you’ll probably have more things to add. Therefore, the overview below serves as an example.

| Single-step P&L statement | Period covered: June 2024 |

|---|---|

| Small bakery: Bread Unlimited | Currency: USD |

| Revenue: Baked goods and beverages sold (A) | 3,000 |

| Costs: Ingredients, utilities, employee wages (B) | 2,500 |

| Net income: Bakery’s profit after deducting costs from revenue (A – B) | 500 |

#2 Example of profit and loss statement: Product/service company

A profit and loss statement isn’t confined to small businesses, like a bakery in Alabama. You can use it for complex organizations as well.

For this example, it’s recommended that you use the accrual method of accounting. The reason is that this method records expenses or revenue after they’ve provided the service — although the company hasn’t received the cash yet.

The accrual method is used for companies that need to get a more detailed overview of their financial performance. In other words — when the stakes are high.

To create a P&L statement for a software company, you first need to consider the revenue from subscriptions or product sales. After that, it’s appropriate to look into costs (COGS), like licensing, hosting, and customer support costs — all leading you to your gross profit. In short, you get the gross profit by deducting COGS from revenue.

Also, you need to consider the staff’s salaries, rent, and marketing expenses — all operating expenses. When you’re done with that, you need to evaluate the operating profit by deducting operating expenses from gross profit. The next step is to examine your taxes, interest on loans, and other necessary expenditures — your non-operating items.

Finally, you get the net profit — that is, the final figures showing you how well your business is performing.

To make it even more concrete, here’s a simplified breakdown of a multi-step P&L statement you could use for a software company — let’s call them InvincibleDevs.

| Multi-step P&L statement | Period covered: Q1 2024 |

|---|---|

| Software company: InvincibleDevs | Currency: USD |

| Revenue: Subscriptions (or product sales) | 10,000 |

| Costs: Licensing, customer support, software development | 3,000 |

| Gross profit: Revenue – costs | 7,000 |

| Operating expenses: Salaries, office rent, marketing | 5,000 |

| Operating profit: Gross profit – operating expenses (A) | 2,000 |

| Non-operating items: Taxes, interest on loans, depreciation, amortization, etc. (B) | 500 |

| Net income (or net loss): A – B, the final financial result after deducting non-operating items from operating profit | 1,500 |

#3 Example of profit and loss statement: Restaurant

With millions of restaurants spread throughout the world, it might be interesting to explore how a P&L statement can impact their profitability.

For illustration, we can take a single month’s worth of meals and pull it through a comparative P&L statement. In particular, let’s do a summary of the revenue and costs for January and February 2024. For this example, it’s best to use the cash method of accounting, as accountants typically record revenues and expenses only when the cash changes hands.

First, all the meals you typically sell during a month amount to your revenue. After you deduct the cost of goods sold — like ingredients — and labor costs from the revenue, you get a gross margin. Bear in mind that the cost of goods sold and labor costs are often jointly referred to as prime cost.

Second, you need to subtract the operating expenses, including wages of the entire kitchen and wait staff, plus the rent. These expenses are typically fixed.

Third, you have to cover the utilities, marketing expenses, and depreciation — all represented as general and administrative expenses (often also called non-operating expenses).

In the end, our imaginary restaurant is left with the net income on that single month’s worth of meals for January and February 2024.

To make it more concrete, here’s what the restaurant budget for a single month’s worth of meals may look like in a comparative P&L statement:

| Comparative P&L statement | January 2024 | February 2024 |

|---|---|---|

| Restaurant: Palate Paradise | Currency: USD | Currency: USD |

| Revenue: Meals and beverages sold (A) | 1,000 | 950 |

| Cost of goods sold (COGS): Food and ingredients (B) | 200 | 220 |

| Labor costs: Wait and kitchen staff salaries, payroll taxes (C) | 220 | 220 |

| Gross margin: A – B — C | 580 | 510 |

| Operating expenses: Rent | 290 | 290 |

| General and administrative expenses: Depreciation, utility charges, marketing | 220 | 240 |

| Net income: Restaurant’s profit after deducting all costs and expenses from revenue | 70 | –20 |

🎓 Clockify Pro Tip

Speaking of managing restaurants, here’s a list of the 10 of the best management software to operate any restaurant:

3 Tested tips to make better P&L statements

As a business owner, it’s sometimes difficult to remember to do everything that needs to be done — from paying employees and contractors to recording and submitting all the required information to the authorities.

That’s why we’ve laid out 3 simple yet effective ways to make your profit and loss statements more akin to a walk in the park.

Tip #1: Track your time to better manage labor costs

You can’t possibly know everything that’s going on in your business if you don’t track what and when employees are doing. So, to improve your bottom line, you’ll have to keep tabs on the labor cost of people involved in your company.

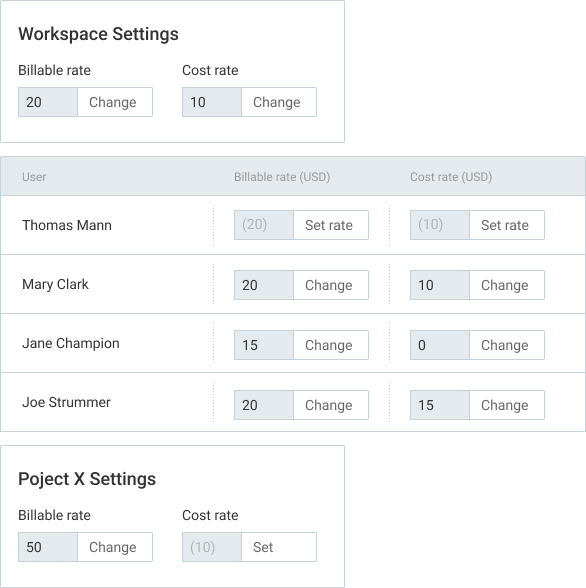

For example, a time-tracking system like Clockify lets you add billable rates for your clients — and define cost rates for your workforce. In Clockify reports, you get to compare your billable amounts (what you charge your clients) with your cost amounts (what you pay your employees).

As a result, you can better track profitability.

As soon as you enable cost rates in Workspace settings, you can apply billable rates and cost rates to any project, client, and employee. This allows you to create more detailed profit and loss statements because you’ll know exactly how much you charge your clients and pay your workforce.

So, the next time you want to make sure you’re meeting your financial goals, remember to start tracking your productivity and doing the same for your employees. Doing so will help you see where time is slipping through the cracks — and thereby ruining your business.

Tip #2: Keep tabs on expenses to protect your bottom line

A study that surveyed more than 200 Nordic organizations found that around 20% of receipts don’t make it into expense reports. That’s a sad reality for many companies nowadays. Yet, the cure to this problem is simple: Digitize your receipts!

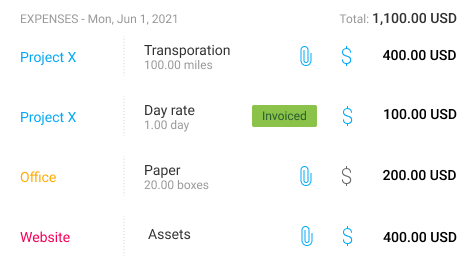

For example, you can use an expense-tracking app like Clockify to track costs for project fixed fees by categories, like sum or unit. After inserting expenses, Clockify generates a fitting invoice that reflects all the expenses by category.

To tie it up with your P&L statement, you can track how much your team is spending on operating expenses, like marketing or purchasing office supplies.

In fact, you can organize your expenses per many items, including:

- Team member,

- Date,

- Project,

- Category, and more.

🎓 Clockify Pro Tip

Whether you work as an accountant or just want to get a head start on tracking your expenses, check out our informative article on this topic:

Tip #3: Manage your time better to increase productivity

This point bears repeating in any sector — create an impenetrable time management system.

If your accountants and workforce are exhausted, they can make errors in their work, including what goes into your P&L statement.

But suppose you decide to make time management a priority. In this case, one of the intended consequences will be an improvement in your company’s bottom line.

So, here are a few practical tips for managing your time well when crafting a P&L statement:

- Type in the title of your task in your time-tracking app,

- Click on the dollar sign to mark your time as billable,

- Start the timer to track your billable hours,

- Record expenses in your dedicated time billing software, and

- Create invoices for the services you provided.

As soon as you implement these techniques, you’ll be on your way to creating better financial statements and a work environment that drives stellar performance.

🎓 Clockify Pro Tip

Get bite-sized advice on how to manage your time even better in our comprehensive guide:

Profit and loss statement templates

Now you have everything you need to grow your knowledge about P&L statements. But it’s prime time we get to a few useful templates you can use to craft your own profit and loss statement.

In this section, we’ll look into 3 templates of profit and loss statements:

- Single-step P&L statement template,

- Multi-step P&L statement template, and

- Comparative P&L statement template.

We hope you’re excited as we are — let’s dig in!

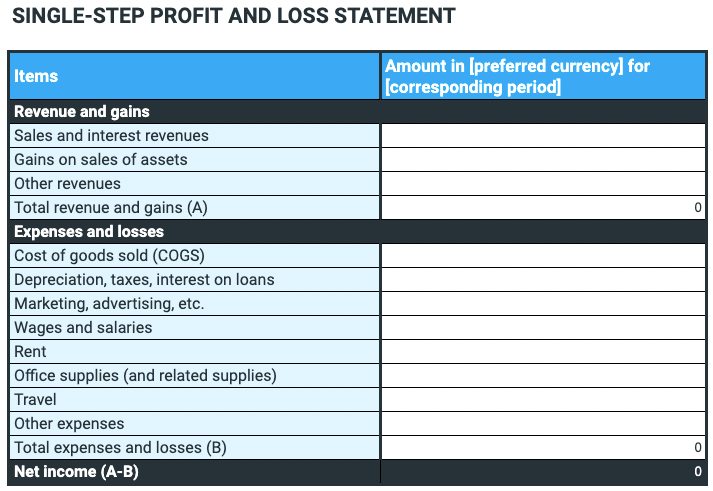

Profit and loss template #1: Single-step P&L statement

The single-step P&L statement is a simple financial tool that lets you get a bird’s-eye view of how much money your business is making or losing. Yet, its use doesn’t spread beyond small businesses — like our small bakery in Alabama. Larger companies typically avoid this when making long-term decisions.

The Single-step P&L statement template is useful if you’re just starting out and you’d like to calculate your total income without having to create a single-step P&L statement from scratch.

This template is also practical for getting a snapshot of your expenses and cost of goods sold. In fact, it’s called single-step because it gives you a picture of the loss or profit in a single step. Yet, it doesn’t list things like operating and non-operating costs — things that still impact the bottom line.

Pros of the Single-step P&L statement template:

- Makes record-keeping easy due to its simplicity, and

- Focuses on the company’s financial bottom line.

Cons of the Single-step P&L statement template:

- Doesn’t distinguish between operating costs and non-operating costs, and

- Makes it hard to determine the sources of many activities, which discourages investors from investing in the business.

How best to use the Single-step P&L statement template?

You have 2 formats to choose from for your template: a Google Sheets file and an Excel spreadsheet.

If you click on the Google Sheets link below, a new screen will appear with the prompt: Would you like to make a copy of the Single-step P&L statement template?

Click on Make a copy, and you’ll get an editable copy of the Single-step P&L statement template.

If you go with the Excel spreadsheet, clicking on the link will save the document to your device.

In any case, the document will be empty, with many zeroes. As soon as you begin inserting your digits, it will start to take shape.

After you’ve inserted your company’s details and the period you want to cover, start by filling in the Revenue and gains column by adding details such as:

- Sales and interest revenues,

- Gains on sales of assets, and other revenues.

Next, you need to populate data in the Expenses and losses column, including:

- Cost of goods sold,

- Depreciation,

- Wages,

- Office supplies,

- Rent, and other expenses.

To get the net income, you’ll need to subtract the Total of expenses and losses from the Total revenue and gains.

⬇️ Download the Single-step P&L statement template (Google Sheets)

⬇️ Download the Single-step P&L statement template (Excel)

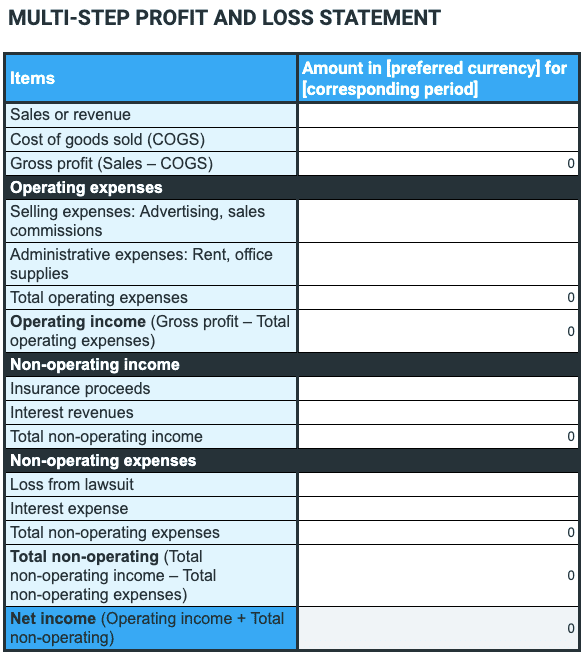

Profit and loss template #2: Multi-step P&L statement

The multi-step P&L statement is a more detailed type of profit and loss statement that includes multiple subtotals. For example, it separates the operating expenses and operating income from non-operating expenses and non-operating income. In turn, this helps a company find out which areas are performing as expected or poorly.

Suppose a budget item from your non-operating income — like insurance proceeds — is through the roof. In this case, the multi-step P&L statement provides you with details about this item. In contrast, the single-step P&L statement typically attaches this non-operating income to other budget items, which doesn’t give a proper explanation for the rise in insurance proceeds.

Filing out this template is time-consuming, but it helps you get more in-depth into your financial situation and is meant for mid-sized and large businesses.

Pros of the Multi-step P&L statement template:

- Calculates gross profit and operating income easily, and

- Offers deeper insight into operating trends and financial performance.

Cons of the Multi-step P&L statement template:

- Lacks simplicity, making it hard for non-finance persons to interpret, and

- Takes plenty of time and effort to create one.

How best to use the Multi-step P&L statement template?

You have 2 formats to choose from for your template: a Google Sheets file and an Excel spreadsheet.

If you click on the Google Sheets link below, a new screen will appear with the prompt: Would you like to make a copy of the Multi-step P&L statement template?

Click on Make a copy, and you’ll get an editable copy of the Multi-step P&L statement template.

If you go with the Excel spreadsheet, clicking on the link will save the document to your device.

In any case, the document will be empty, with many zeroes. As soon as you begin inserting your digits, it will start to take shape.

After you’ve inserted your company’s details and the period you want to cover, start by filling in details such as:

- Sales or revenue, and

- Cost of goods sold.

Next, you need to populate data in the Operating expenses column, including:

- Selling expenses, and

- Administrative expenses.

This brings you to the Operating income, which you get when you subtract Total operating expenses from your Gross profit. The line item Operating income is critical, as it lets you see if your operating activities are generating profit or not. Depending on the industry, an operating activity can fall into many categories, like manufacturing, sales, marketing, and others.

Next, you need to fill in data for:

- Non-operating income, and

- Non-operating expenses.

To get the net income, you’ll need to add Operating income to the Total non-operating expenses. For simplicity’s sake, net income is the bottom line of a company. In other words, it represents the amount your business has made after deducting expenses, taxes, allowances, and other costs.

⬇️ Download the Multi-step P&L statement template (Google Sheets)

⬇️ Download the Multi-step P&L statement template (Excel)

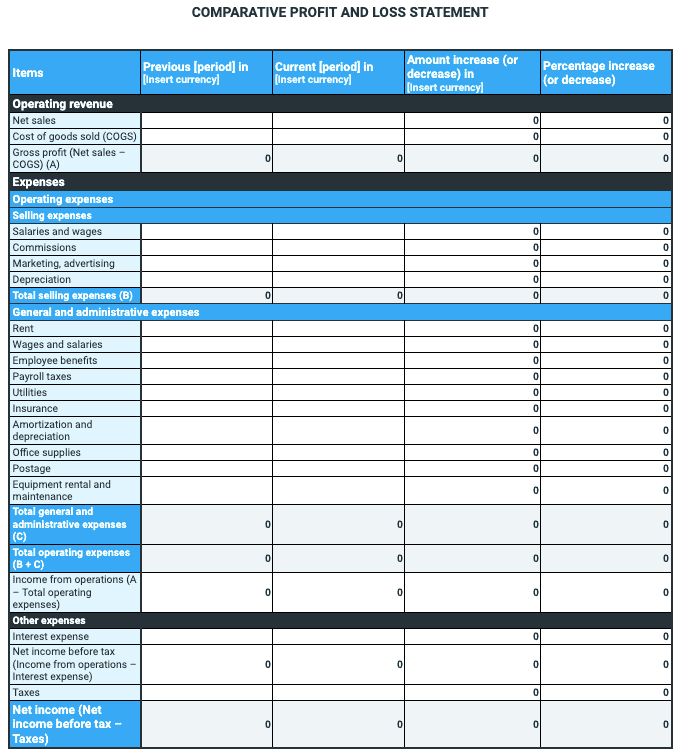

Profit and loss template #3: Comparative P&L statement

The comparative P&L statement is a complex type of a profit and loss statement that compares different accounting periods for one company — or multiple different-sized companies. Experts praise it as one of the most useful P&L statements, as it presents investors and managers with changes in percentage and numbers from one period to the next.

The Comparative P&L statement template presents figures of expenses and income on a single page without having to go back to previous P&L statements and compare them to current ones.

This template allows you to spot problems and trends over different accounting periods. In fact, since it’s digital, you can easily correct numbers and do necessary calculations online without having to print them out.

Pros of the Comparative P&L statement template:

- Provides a clear comparison between multiple accounting periods, and

- Simplifies analysis of sales and net income line items.

Cons of the Comparative P&L statement template:

- Benefits the company only if it uses identical accounting principles consistently to produce such P&L statements (like the accrual or cash method), and

- Fails to be practical when the company branches out into new lines of business.

How best to use the Comparative P&L statement template?

You have 2 formats to choose from for your template: a Google Sheets file and an Excel spreadsheet.

If you click on the Google Sheets link below, a new screen will appear with the prompt: Would you like to make a copy of the Comparative P&L statement template?

Click on Make a copy, and you’ll get an editable copy of the Comparative P&L statement template.

If you go with the Excel spreadsheet, clicking on the link will save the document to your device.

In any case, the document will be empty, with many zeroes. As soon as you begin inserting your digits, it will start to take shape.

After you’ve inserted your company’s details and the period you want to cover, start by filling in details for the Operating revenue column, such as:

- Net sales, and

- Cost of goods sold.

Next, you need to populate data in the Operating expenses and General and administrative expenses columns, including:

- Salaries and wages,

- Marketing,

- Depreciation,

- Rent,

- Payroll taxes,

- Insurance, and others.

This brings you to the Total operating expenses column, which you get when you add Total selling expenses to the Total general and administrative expenses.

Next, you need to fill in data for:

- Income from operations,

- Interest expenses,

- Taxes, and others.

To get the net income, you’ll need to subtract Net income before tax from Taxes.

⬇️ Download the Comparative P&L statement template (Google Sheets)

⬇️ Download the Comparative P&L statement template (Excel)

—

Note: Even though our P&L statement templates are pretty straightforward, it’s always best to consult with an accountant before making a profit and loss statement official. Clockify is not responsible for any losses or risks incurred should this example be used without further guidance from professionals.

FAQ about profit and loss statements

In this segment, we’ll take a look at a few frequently asked questions people face when they start working on a profit and loss statement.

What is the difference between a cash flow statement, balance sheet, and P&L?

Companies typically make 3 types of financial statements on their financial performance annually, quarterly, and monthly, including:

- Cash flow statement — a financial document that lists the sources of cash deriving from investment, operating, and financing activities,

- Balance sheet — a financial statement that looks into equity, liabilities, and assets that the company has in its possession, and

- Profit and loss statement or income statement — a financial document that details revenues, sales, expenses, and costs in one form or another, depending on the company’s reporting standards.

But when it comes to disclosing this information, not all companies have the same responsibilities toward authorities.

Which companies have to give away financial statements?

Public companies are required by law to file regular reports with the U.S. Securities and Exchange Commission. Yet, most private companies don’t have to disclose this information — at least the ones with less than $10,000,000 in assets and with more than 500 owners who hold securities (a financial instrument that provides individuals with a form of company ownership).

Private companies that aren’t subject to these criteria often still provide these financial statements to the authorities. The reason? Well, this information gives financial experts deeper insight into how they do business. As a result, investors can make informed decisions about investing, and buyers can decide whether they want to buy or sell a company.

Paired together, the cash flow statement, balance sheet, and profit and loss statement comprise 3 critical components that help managers and investors explore a company’s financial performance over a given accounting period.

Is a P&L the same as an income statement?

Yes, profit and loss statement and income statement are synonyms for the financial document that gives you insight into your company’s financial performance. They include expenses, revenue, and net profit for a given accounting period (a week, month, quarter, or year).

Is P&L the same as a balance sheet?

A profit and loss statement differs from a balance sheet by focusing on expenses and revenue. On the other hand, the balance sheet looks into:

- Liabilities,

- Assets, and

- Equity.

Yet, the balance sheet is a critical companion of the P&L statement in assessing the overall health of a business.

Does P&L include revenue?

Yes, a profit and loss statement always includes revenue and expenses. Line items on revenue, sales, expenses, and costs are the identifying marks of P&L statements.

Is a P&L a cash flow statement?

No, a profit and loss statement isn’t the same as a cash flow statement. Unlike the P&L statement, the cash flow statement lists the cash sources stemming from investment activities, operating activities, and financing activities. In other words, the cash flow statement doesn’t include information on expenses and revenue — as is the case with the P&L statement.

Wrap-up: Prepare regular P&L statements to learn if your business operations are profitable

To make your profits shine, you surely have to go through a strenuous process. And it’s so much more than mere cost management!

In fact, you need to be aware of what exactly happens with your company’s money — and this is where a profit and loss statement comes into play.

In a nutshell, P&L statements allow accountants and managers to make more informed decisions by giving them insight into which activities are a waste of money and which generate profit.

For this and a wealth of other reasons, we geared you up with everything that can help you make the best profit and loss statements, paired with examples and templates.

In summary, here are the main takeaways:

- Choose a simple or complex type of a P&L statement, depending on your needs,

- Harness the power of expense-tracking software to make the process effortless,

- Use templates to speed up the creation of a P&L statement,

- Implement a P&L statement regularly to keep tabs on sales and revenues, and

- Track and manage your time by using time and billing software.

If you follow just a few of these pieces of advice, you’ll be on your way to creating profit and loss statements that will amaze investors and managers alike.

Sources for the table:

- Khatabook, Comparative Income Statement: Examples, Analysis and Format

- Library of Congress, Research Guide on U.S. Private Companies

- Millie Atkinson, 2017, Income Statements Essentials

- Risks and benefits of handling digital receipts, Eurocard, 2021

- Sandy Baruffi, 2021, The Basics Of Understanding Financial Statements: A Guide To Understanding Financial Reports

- U.S. Securities and Exchange Commission, The Laws that Govern the Securities Industry

- U.S. Securities and Exchange Commission, What does it mean to be a public company?

- WallStreetMojo, Single-step Income Statement